A Guide to SPVs

What is a special purpose vehicle? A quick guide

Ever heard the term Special Purpose Vehicle (SPV) and wondered what it is? It's a key tool in finance, but the concept is simpler than it sounds. At its heart, an SPV is a separate legal company created by a parent company to wall off financial risk.

Think of it as a financial quarantine zone. It’s a distinct, secure container built to hold specific assets or liabilities for a single, focused mission, like a massive infrastructure project or a complex securitization deal. This structure makes sure the SPV’s financial fate is completely separate from the parent company's balance sheet.

What Is a Special Purpose Vehicle

Let’s play this out. Imagine a big real estate developer wants to build a cutting-edge skyscraper. It’s a project with huge potential but also massive financial risk. If it flops, the losses could sink the entire company.

So, what do they do? To protect the mothership, the developer sets up an SPV.

This new entity—sometimes called a Special Purpose Entity (SPE) or a Special Purpose Company (SPC)—is legally independent from its parent. The developer transfers all the assets, contracts, and financing related to the skyscraper project into this SPV. Now, the project has its own dedicated legal and financial bubble.

The Financial Firewall

The whole point of this exercise boils down to one critical concept: "bankruptcy remoteness." This is the legal firewall that makes an SPV so powerful.

It guarantees that if the skyscraper project goes south and declares bankruptcy, its creditors can only go after the assets held inside that specific SPV. They can't touch the parent company's other properties, its cash reserves, or any of its other ongoing projects. The firewall holds.

To get a better handle on the core idea, let's break down the essential features of an SPV.

Key Characteristics of a Special Purpose Vehicle

| Characteristic | Explanation |

|---|---|

| Legal Separation | It's a legally distinct entity (LLC, corporation, trust) from its parent company. |

| Specific Purpose | Its operations are strictly limited to a single, defined mission or transaction. |

| Asset Isolation | It holds specific assets (and related liabilities) separate from the parent's balance sheet. |

| Bankruptcy Remoteness | Designed to be unaffected by the parent company's financial distress or bankruptcy. |

| Off-Balance-Sheet | Often structured so its assets and debts don't appear on the parent's primary financials. |

This structure is a game-changer for managing risk and unlocking financing.

While construction and logistics have their own heavy-duty special purpose vehicles, in finance, the term describes these precisely engineered legal entities. And it's big business. The global market for these financial SPV services was valued at around $0.67 billion in 2024 and is on track to more than double, hitting $1.55 billion by 2033. You can explore more data on this market growth to see just how critical these structures have become.

An SPV is essentially a financial tool that allows a company to pursue a high-risk, high-reward venture without betting the entire farm. It isolates the venture's success or failure, protecting the core business from potential fallout.

Don't mistake an SPV for just another subsidiary. It's a surgical instrument. Its governance, operations, and entire reason for being are tightly restricted to the specific mission it was born to accomplish. That sharp focus and legal separation are what make it an indispensable tool in modern global finance, powering everything from real estate developments to complex asset-backed securities.

Why Businesses Create Special Purpose Vehicles

Knowing what an SPV is only gets you halfway there. The real question is why companies go through all the trouble of setting up these distinct legal entities in the first place. The answer isn't just academic; it’s about strategic financial engineering, usually aimed at managing risk or opening up money-making avenues that would otherwise be locked away.

Think of it as a defensive move. Companies use SPVs to build a financial fortress around a specific asset or project. It’s a deliberate strategy to make sure one bad bet doesn't bring down the whole house. This simple idea is the driving force behind almost every SPV you'll encounter.

The Power of Risk Isolation

The single biggest reason to create an SPV is risk mitigation. It’s all about containing the blast radius.

Imagine a huge corporation wants to fund a billion-dollar deep-sea drilling project. The upside is massive, but the potential for financial, environmental, and legal disaster is just as big. It's a high-stakes gamble.

So, what do they do? They spin up a new SPV and stick the entire project inside it—the assets, the financing, all of it. If the project goes south and racks up huge liabilities, creditors can only go after the assets held within that specific SPV. The parent company's core operations are shielded. This is the whole point of making an SPV "bankruptcy-remote."

A special purpose vehicle allows a company to quarantine risk. It's like putting a volatile experiment in a sealed, reinforced lab; if something goes wrong, the explosion is contained and doesn't destroy the entire building.

This separation gives companies the breathing room to chase ambitious, high-reward projects that would simply be too dangerous to put on their main balance sheet.

Transforming Illiquid Assets into Cash

Another huge driver for creating SPVs is asset securitization. This is all about turning long-term I.O.U.s into immediate cash.

Banks and lenders, for example, have balance sheets packed with assets like mortgages, auto loans, and credit card debt. These things are valuable and generate steady income, but the cash is tied up for years. An SPV is the perfect tool to unlock that value.

Here's how it generally plays out:

- Asset Transfer: The parent company (the "originator") sells a massive pool of these loans to a brand-new special purpose vehicle.

- Issuance of Securities: The SPV now legally owns the income stream from all those loans. It then bundles them up and issues tradable bonds (securities) to investors on the open market.

- Capital Infusion: The cash from selling those bonds flows right back to the parent company. Boom—instant liquidity.

This clever process turns a pile of non-tradable loans into cold, hard cash. The investors who bought the bonds get paid from the loan payments flowing into the SPV. Meanwhile, the parent company has moved the assets and their risks off its books and now has a big pile of capital to fund new loans or other ventures.

Other Strategic Financial Objectives

Beyond walling off risk and turning loans into cash, SPVs are financial multi-tools. Companies pull them out of the toolbox for all sorts of specific, targeted goals.

Often, it's about creating a clean, simple structure for a messy transaction. This makes the deal far more appealing to investors or partners who might not want to get entangled in the complex financial web of a massive corporation.

Some other common uses include:

- Project Financing: SPVs are the go-to structure for massive infrastructure projects—think toll roads, power plants, or bridges. The SPV owns the project and gets financing based only on the project's future cash flow, keeping all that debt off the sponsors' balance sheets.

- Property Acquisition: When buying real estate, an SPV can make things much simpler. For instance, if property sale taxes are sky-high, a company might put the property into an SPV and then just sell the shares of the SPV. This move can sometimes get taxed at a lower capital gains rate.

- Joint Ventures: When two or more companies team up, an SPV acts as a clean, neutral home for the venture. It clearly spells out each partner's contributions, ownership, and liabilities without muddying the financial waters of the parent companies.

The Legal and Structural Blueprint of an SPV

A Special Purpose Vehicle isn't just a shell company on paper; it's a carefully engineered financial structure built for a single, focused job. Its entire effectiveness hangs on a very specific legal and operational blueprint, one designed to keep it independent, solvent, and trustworthy in the eyes of investors.

The whole point is to create an entity that can stand on its own two feet, legally and financially walled off from its parent company. This doesn't happen by chance. It takes very specific legal firewalls, minimalist governance, and mechanisms that give investors the confidence to put their money in. Let's pull back the curtain on how these things are actually built.

The Foundation: Bankruptcy Remoteness

The single most critical feature of any SPV is its bankruptcy remoteness. This is the legal firewall that does all the work. It’s constructed using several non-negotiable legal tools that prevent the SPV from getting sucked into the parent's financial troubles, or vice versa.

Think of it like building a submarine. You don’t just cross your fingers and hope it's waterproof. You engineer it with specific seals, a reinforced hull, and totally independent life support systems. An SPV is built with the same kind of legal reinforcements to make sure it stays isolated.

Here are the key elements that make it happen:

- Independent Directors: An SPV’s board will almost always include one or more independent directors with zero affiliation to the parent company. Their legal duty is to the SPV alone, and they must approve any huge decisions, like filing for bankruptcy. This is a critical check that stops a struggling parent from pulling the plug on a healthy SPV just to serve its own needs.

- Restrictive Covenants: The SPV’s legal charter is packed with strict rules, or covenants, that severely tie its hands. It can’t just go out and take on new debt, merge with another company, or sell off its core assets. This keeps its mission pure and its financial condition completely predictable.

- Separateness Covenants: These clauses force the SPV to act like a totally separate business. We're talking its own letterhead, its own bank accounts, its own financial statements. It has to conduct all business with its parent at arm's length. This is what prevents a judge from "piercing the corporate veil" and lumping the SPV's assets in with the parent's during a bankruptcy.

Lean Governance and a Laser-Focused Mission

A normal company is built for growth and change. An SPV is the polar opposite. Its mission is incredibly narrow and defined from day one, and its governance structure reflects that laser focus. You won't find a marketing department, R&D teams, or sprawling corporate hierarchies here.

The governance is lean by design, built only to execute its specific task—say, collecting mortgage payments and passing them through to bondholders. This simplicity strips out operational risk and ensures the SPV doesn't wander off-mission. Every single action it can take is spelled out in the transaction's legal documents.

The Role of Credit Enhancements

To make the bonds or other securities issued by the SPV more attractive to investors, dealmakers often add credit enhancements. These are just financial mechanisms that lower the risk for investors by giving them an extra layer of protection against losses.

A credit enhancement is basically an insurance policy for investors. It creates a financial cushion to absorb the first wave of losses if some of the underlying assets go bad, protecting the payments owed to bondholders.

You'll typically see these common forms:

- Overcollateralization: This is the most straightforward method. The SPV simply holds more assets than the value of the securities it issues. For example, an SPV might issue $100 million in bonds backed by a pool of $110 million in auto loans. That extra $10 million is a buffer against defaults.

- Subordination: This is where you create a capital structure with different classes, or tranches, of securities. The senior tranches have first dibs on the cash flows and are the lowest risk. The junior (or subordinated) tranches get paid last, so they take the first hit from any losses, but they offer higher interest rates to compensate for that risk.

- Third-Party Guarantees: Sometimes a bank or an insurance company will step in and provide a guarantee to cover losses up to a certain amount. This adds an external layer of security and can really boost investor confidence.

Finally, an independent trustee—usually a big financial institution—is brought in to act as the guardian for the bondholders. The trustee makes sure the SPV follows all the rules and that investors get paid on time. They provide a crucial layer of oversight that keeps the whole structure transparent and reliable.

SPVs in Action Across Financial Markets

Theory is great, but to really get a feel for the power of a Special Purpose Vehicle, you have to see it in the wild. The legal nuts and bolts are interesting, sure, but the real impact comes to life when you see how SPVs grease the wheels of major financial markets. They're the invisible engines driving a lot of common investment products and high-stakes deals.

SPVs are the essential framework for all sorts of complex transactions, from rolling up a bunch of mortgages into tradable bonds to helping venture capitalists fund the next big startup. Let's walk through a few real-world examples to see exactly how these tools work.

Securitization: The CMBS Example

Commercial Mortgage-Backed Securities (CMBS) are a perfect case study.

Picture a big bank. It’s sitting on a portfolio of hundreds of commercial real estate loans, each tied to a different office building, mall, or hotel. These loans bring in a steady stream of cash, but they're super illiquid—you can't just sell them off for cash on a Tuesday afternoon.

This is where the SPV steps in. The process is pretty straightforward:

- Create and Transfer: The bank sets up a brand new, bankruptcy-remote SPV. Then, it sells the entire pile of commercial mortgage loans to this new entity.

- Issue Bonds: The SPV is now the legal owner of those loans and all the future income they'll generate. It turns around and issues bonds to investors on the open market. These bonds are backed, or "secured," by the mortgage payments flowing from the properties.

- Distribute Cash Flow: As the property owners make their monthly mortgage payments, that money goes directly into the SPV. The SPV’s job is then to pass that cash along to the bondholders as their interest and principal payments.

Just like that, the bank has turned a huge, illiquid loan portfolio into cold, hard cash. At the same time, investors get a way to tap into the commercial real estate market through a security they can easily buy and sell. The SPV is the critical, risk-isolating bridge connecting the two sides.

For example, BANK 2019-BNK16 demonstrates this structure in practice: a $1.4 billion CMBS deal backed by 48 commercial properties, with the SPV (BANK 2019-BNK16 Depositor Inc.) holding the mortgages and issuing multiple tranches of bonds to investors.

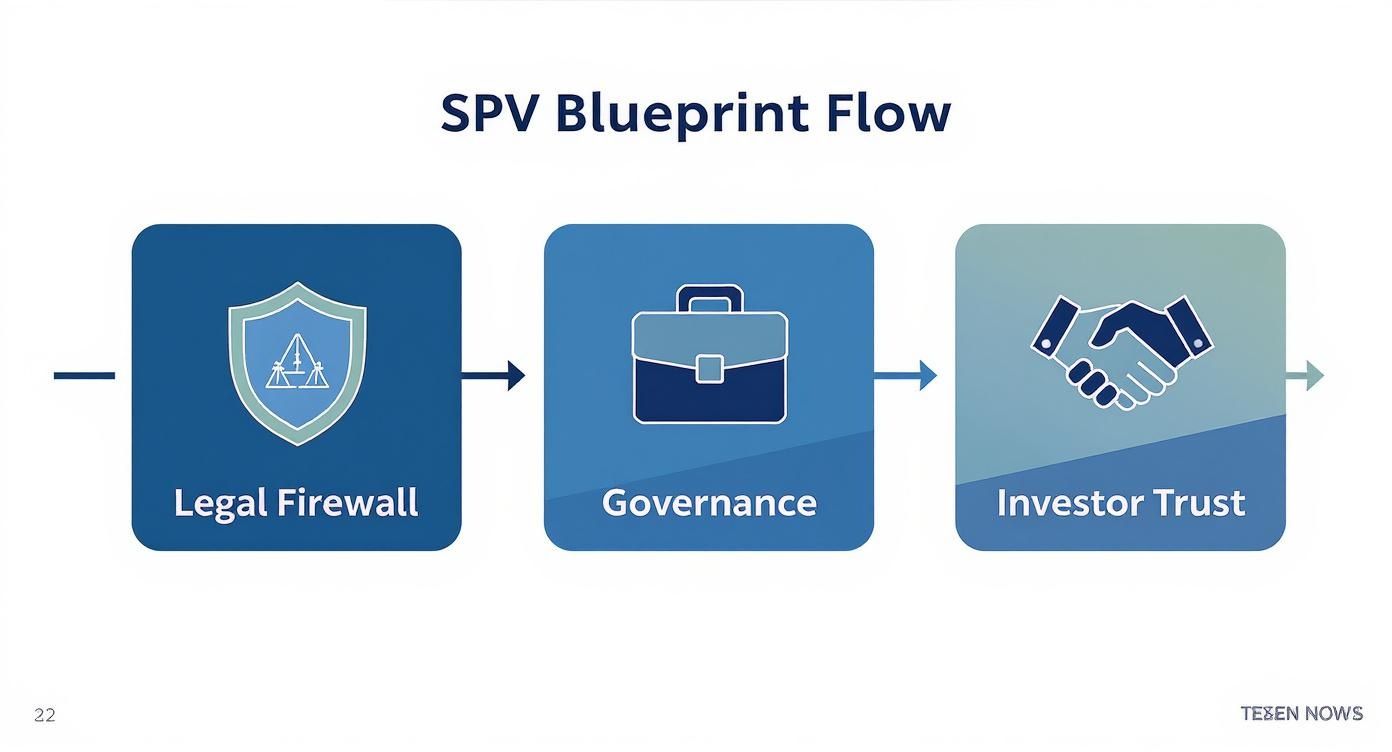

The infographic below shows the basic blueprint. It highlights the legal firewall, dedicated governance, and investor trust that make it all possible.

This flow really shows how an SPV is built from the ground up to be a trustworthy, independent entity. That’s precisely why investors are comfortable buying the securities it issues.

Asset-Backed Securities: Beyond Real Estate

The same basic idea applies to Asset-Backed Securities (ABS), just with different stuff underneath. Instead of commercial mortgages, the SPV might hold a pool of auto loans, student loans, or even credit card debt. The end goal is identical: package up these income-producing assets into securities that can be sold to investors.

In essence, securitization using an SPV is a form of financial alchemy. It transforms thousands of individual, non-tradable debt obligations into a single, uniform, and liquid investment product.

This process is absolutely vital for lenders. It clears their balance sheets so they can go out and make new loans, which helps keep the economy moving. Without the SPV structure, this kind of efficient risk and capital transfer would be a whole lot harder to pull off.

Fueling Growth in Private Markets

Beyond massive securitization deals, SPVs have become a go-to tool in the private equity and venture capital worlds.

When a group of investors wants to pool their money for a single, focused investment—like backing a hot tech startup or buying out a mid-sized company—an SPV is the perfect vehicle.

Instead of every single investor cluttering up the startup's cap table, they all invest through one SPV. That SPV then makes a single, clean investment into the target company. For the startup, this is a lifesaver, dramatically simplifying their legal and administrative headaches.

This approach has absolutely taken off. Data from Carta shows that in Q4 2024, the number of new SPVs created on their platform was up a staggering 116% from just five years earlier. This explosion shows just how much SPVs have become the standard for managing syndicated investments. You can discover more insights about SPV usage in private markets to see the full trend. The structure allows a bunch of investors to get into a single deal while staying legally and financially separate from the deal's sponsor.

Evaluating the Risks and Red Flags of SPVs

A special purpose vehicle is an incredibly powerful tool, but its biggest strengths—complexity and separation—can flip into its greatest weaknesses in a heartbeat. For every legitimate SPV created to nail down risk or smooth out an investment, there’s always the potential for a bad actor to twist it for other means. This kind of financial engineering, if it isn't handled with total transparency, can easily hide a company's true financial health, mislead investors, and even cook up systemic risk.

The very structure that’s designed to wall off risk can just as easily be used to bury it. An SPV lifts assets and, more critically, liabilities right off a parent company's balance sheet. While that’s standard procedure for something like securitization, it can also make a company look a lot healthier and less leveraged than it really is. This was the shell game at the heart of the 2008 financial crisis, where off-balance-sheet entities were used to mask the insane levels of risk banks were actually holding.

Complexity and Opaque Structures

One of the biggest dangers is intentional obscurity. When you see an SPV structure that's absurdly convoluted, with layers of entities sprinkled across multiple jurisdictions, that should set off alarm bells immediately. This kind of complexity isn't always about efficiency; sometimes, it’s a deliberate maze built to make tracing assets and figuring out who's on the hook for what a nightmare.

This was a core feature of the 2008 meltdown. Financial institutions spun up incredibly complex webs of SPVs to package and sell mortgage-backed securities. When the underlying mortgages started to sour, the sheer opacity of these structures made it impossible for investors and regulators to figure out who was exposed and by how much. That confusion lit the fuse for a chain reaction of panic and collapse.

An SPV should simplify a transaction, not complicate it. If the structure seems designed to confuse rather than clarify, it’s a major red flag that something other than legitimate financial engineering is at play.

This is precisely why due diligence is non-negotiable. The only real defense against these hidden risks is a crystal-clear understanding of what an SPV holds, who it owes, and how it all connects.

Regulatory and Reputational Risks

Even when they're set up by the book, SPVs aren't immune to the winds of change from regulators. Accounting standards evolve, and what was once considered off-balance-sheet can suddenly be ordered back onto the parent company's books. This event, known as reconsolidation, can be an absolute disaster.

When reconsolidation hits, the entire rationale for the SPV evaporates overnight. All that debt the parent company thought it had neatly walled off comes roaring back onto its balance sheet. This can easily trigger violations of its own debt covenants and lead to a swift credit rating downgrade. Beyond the numbers, just being associated with a failed or sketchy SPV can do serious damage to a company's reputation, torching the trust it has with its investors and partners.

Critical Red Flags to Monitor

When you're digging into any deal involving an SPV, you have to stay vigilant. There are certain tell-tale signs that can help you separate a standard financial structure from one designed to hide problems. Keeping an eye out for these red flags isn’t just good practice; it’s fundamental to managing your risk.

Here are some of the big ones to watch for:

- Excessive Complexity: A confusing web of interconnected SPVs with no clear business purpose? That's a classic move to obscure ownership or bury debt.

- Unusual Jurisdictions: While many SPVs are legitimately parked in financial hubs for tax neutrality, using a jurisdiction known for extreme secrecy without a compelling reason should make you suspicious.

- Conflicts of Interest: Pay very close attention to the relationships between the parent company, the SPV's management, and its service providers. If the same people are calling the shots for both the parent and the supposedly "independent" SPV, its bankruptcy remoteness is likely a sham.

- Weak Governance: An SPV without genuinely independent directors or with flimsy, poorly defined operational rules is a huge risk. Strong governance is the foundation of its legal separation.

- High Counterparty Risk: Remember, an SPV doesn't operate in a vacuum—it leans on servicers, trustees, and other entities to function. If any of these counterparties are financially weak or have a sketchy track record, the SPV's own stability is on the line.

SPV Due Diligence Checklist

Before getting comfortable with any transaction involving an SPV, a thorough and skeptical due diligence process is essential. It's about asking the hard questions and not stopping until you get clear answers. This checklist provides a solid framework for kicking the tires on an SPV structure.

| Due Diligence Area | Key Questions to Ask |

|---|---|

| Purpose & Business Rationale | Why was this SPV created? Does the stated purpose align with the structure? Is there a clear, logical economic reason for its existence? |

| Legal Structure | Is it a trust, LLC, or corporation? Is the jurisdiction appropriate? Who are the legal advisors, and what is their reputation? |

| Bankruptcy Remoteness | How strong are the separateness covenants? Are there independent directors? Are there any signs of commingling assets or operations with the parent? |

| Asset Quality | What specific assets are held by the SPV? How were they valued? Has an independent appraisal been conducted? |

| Governance & Management | Who is on the board? Are they truly independent? What are their qualifications? How are key decisions made and documented? |

| Counterparty Risk | Who are the servicers, trustees, and credit enhancers? What is their financial health and track record? What happens if one of them fails? |

| Documentation Review | Have you reviewed the offering memorandum, pooling and servicing agreement (PSA), and trust indenture? Do the documents match the stated purpose? |

| Financial Health & Liabilities | What are the SPV's liabilities? Are there any hidden or contingent obligations? Who are the creditors, and what are their rights? |

Think of this checklist as your starting point. Each question will likely lead to more questions, but following this path is the best way to uncover hidden risks and ensure you're not walking into a structure designed to fail.

How to Investigate an SPV's Financial Trail

Knowing the theory behind a special purpose vehicle is one thing. Actually tracing its real-world financial footprint is something else entirely. It’s time to move past the textbook definitions and get your hands dirty. With the right approach, you can peel back the layers and see the assets, counterparties, and money flows that really make an SPV tick.

For any publicly registered security, including those spit out by an SPV, your first stop is always the U.S. Securities and Exchange Commission's EDGAR database. This is the public library of corporate finance, holding the foundational documents that spell out exactly what you're looking at.

Starting with Public Filings

The document you’re hunting for is the prospectus or offering circular. Think of it as the official blueprint for the entire deal. It details everything from the assets stuffed into the SPV to the names of the trustee and servicer. To find it, you need to search for the SPV or the deal itself.

EDGAR's search interface lets you look up companies, funds, and individuals.

Just punch in the name of the issuing entity—the SPV—and you'll pull up a list of its public filings. The prospectus is your Rosetta Stone.

Once you have that document, you can start mapping out the structure. It will explicitly name all the key players involved:

- The Originator: The parent company that cooked up the SPV and dropped the assets into it.

- The Trustee: The financial institution supposedly looking out for the interests of the bondholders.

- The Servicer: The entity hired to do the day-to-day work, like collecting loan payments.

These relationships are the skeleton of the whole operation. Identifying each party is just the first step. The real work is researching their financial health and track record independently. That’s how you start to assess counterparty risk.

Tracing Connections and Cash Flows

With the names of the key players in hand, you can start to visualize how they're all connected. This is where specialized financial data platforms come in. A tool like Dealcharts can take that raw public filing data and show you how entities are linked across dozens, or even hundreds, of different deals. Suddenly, you get a much clearer picture of the entire ecosystem.

Investigating an SPV is like a bit of financial archaeology. The prospectus is your map, and each named counterparty is a new site to dig into. By following the trail, you can reconstruct the entire structure and see where the real risks are buried.

This process turns abstract knowledge into a practical skill. You're no longer just reading about what a special purpose vehicle is; you're actively dissecting one.

By following the financial trail from public filings to counterparty analysis, you can see past the legalese and understand the true purpose, asset quality, and cash flow mechanics of any SPV you come across. This is what real due diligence in structured finance looks like.

A Few Common Questions About SPVs

Even when you get the mechanics, the whole idea of an SPV can feel a bit counterintuitive. Let's tackle a few of the most common questions that come up.

Is an SPV the Same Thing as a Shell Company?

Not really, though I see why people make the connection. They can look similar from the outside, but it all comes down to intent.

An SPV is built for a specific, legitimate, and transparent financial job, like holding mortgages for a securitization deal. Everything it does is spelled out for investors and regulators. A "shell company," on the other hand, usually has a shadier vibe—it’s often a tool to obscure who owns what, sometimes for reasons you wouldn't want to explain to a judge. The real difference is legitimate business purpose and transparency.

So, Who Actually Owns the Thing?

This is where it gets a little weird, but it’s by design. The ownership is structured to ensure the SPV is truly independent from the company that created it.

Often, an SPV is technically owned by an independent third party, like a trust. This is a crucial step to keep the assets (and debts) off the parent company's balance sheet. But the parent company—the "originator" that sold the assets to the SPV in the first place—is usually the one with the main economic stake in the game. And the investors? They aren't buying shares of the SPV itself; they're buying securities that give them a right to the cash flow from the assets inside the SPV.

Why Are So Many SPVs Based in Places Like the Cayman Islands?

It’s a fair question. You see a ton of these entities set up in jurisdictions like the Cayman Islands, Luxembourg, or Dublin. But it’s less about secrecy and more about financial and legal efficiency.

These locations are picked for their stable, predictable legal systems and, importantly, their tax neutrality. You don't get extra layers of tax slapped on the SPV's transactions, which keeps the financial plumbing clean and simple for a global pool of investors.

It’s all about creating a predictable, efficient path for cash to flow from the underlying assets to the investors, no matter where they are in the world. Making the investment straightforward and attractive is the name of the game. An SPV's address isn't an accident; it's a strategic choice.

Article created using Outrank