Defeasance Guide

A Practical Guide to Defeasance in Real Estate

Defeasance is a process that allows a real estate owner to release a property from the lien of a loan before its maturity date. It involves substituting the real estate collateral with a portfolio of government securities. This mechanism is almost exclusively associated with Commercial Mortgage-Backed Securities (CMBS) loans, which typically prohibit traditional prepayment.

The objective of defeasance is to enable the sale or refinancing of a property that is encumbered by a loan with strict prepayment restrictions.

The Purpose of Defeasance

Many commercial real estate loans, particularly those securitized in CMBS transactions, are structured to prevent early repayment. The investors who purchase CMBS bonds rely on a predictable stream of income over a specified term. An unscheduled loan payoff disrupts this income stream and negatively impacts bondholder returns.

Defeasance addresses this structural issue. Instead of repaying the loan principal, the borrower acquires a portfolio of government securities. This portfolio is structured to generate cash flow that precisely matches all remaining loan payments—both principal and interest—through the original maturity date.

The original loan remains outstanding but is now secured by the portfolio of government bonds rather than the real property. From the perspective of the CMBS bondholders, the expected payment stream is preserved, now backed by low-risk government obligations. The investors are made whole.

Why Prepayment is Often Prohibited

The structure of CMBS is the primary reason prepayment is not an option. These loans are pooled, tranched, and sold to investors who require a specified yield over a defined period. To ensure this, loan agreements include significant barriers to early repayment:

- Lockout Periods: A defined term at the beginning of the loan during which any form of prepayment is strictly prohibited.

- Prepayment Penalties: After the lockout period, mechanisms like "yield maintenance" impose substantial fees designed to compensate investors for lost interest from an early payoff.

Defeasance serves as a structured alternative. By substituting the collateral, the borrower removes the loan's lien from the property, which can then be sold or refinanced. The original loan continues to exist, secured by the new securities portfolio, satisfying the requirements of the CMBS trust. The prevalence of these structures can be observed in data on recent CMBS issuances.

Key Takeaway: Defeasance is a collateral substitution, not a loan payoff. The loan and its payment schedule remain intact for investors, while the borrower frees the real estate asset.

The process provides necessary flexibility for borrowers while preserving the stable, long-term returns required by CMBS investors. Understanding this dual function is essential to grasping why defeasance in real estate is a critical mechanism in structured finance.

The Step-by-Step Defeasance Transaction Process

When a property needs to be sold or refinanced but is encumbered by a CMBS loan with prepayment restrictions, the defeasance process is initiated. It is a collateral swap, trading the real estate for a portfolio of government securities that guarantees the bondholders' expected cash flows. The process is a structured, multi-stage transaction requiring precision.

The borrower's first step is typically to engage a specialized defeasance consultant. The consultant coordinates the transaction, managing communication and execution among the various parties, including lawyers, accountants, the loan servicer, and securities brokers.

The fundamental concept is the substitution of one asset for another to release the property from the loan's lien.

The loan itself is not extinguished; it is assigned a new, highly rated form of collateral, which allows the real estate to be released.

The Defeasance Quote and Portfolio Construction

The consultant begins by preparing a defeasance quote. This involves analyzing the loan documents and calculating the precise remaining payment schedule. This calculation forms the basis for the entire transaction.

The consultant then works with a securities broker to identify the most cost-effective portfolio of U.S. Treasury securities or other eligible government-backed instruments. The portfolio must generate cash flows that perfectly match the loan's remaining payment stream, including all interest, principal, and the final balloon payment. The acquisition cost of this securities portfolio represents the largest expense in the transaction.

Defeasance is a financial engineering exercise. The objective is to construct a securities portfolio that perfectly replicates the loan's payment stream, thereby satisfying the terms of the loan agreement.

Legal and Financial Execution

With the required securities identified, the legal mechanics proceed. A key component is the formation of a successor borrower. This is a new, single-purpose entity created solely to acquire the securities portfolio and assume the loan obligations.

The borrower transfers the funds for the securities purchase to this new entity. The successor borrower then acquires the bonds and legally assumes the role of the obligor on the loan. This legal substitution is what releases the original borrower from the loan obligations.

The process typically requires 30 to 90 days to complete. In addition to the portfolio cost, the borrower is responsible for legal, accounting, and consulting fees, which generally range from 1.5% to 3% of the loan balance. Additional context on the lending market and defeasance costs on chathamfinancial.com can provide further insight.

Final Approvals and Closing

Throughout the process, the loan servicer, acting on behalf of the CMBS trust, oversees and must approve each step. This includes the formation of the successor borrower, all legal documentation, and the final securities portfolio. No part of the transaction can proceed without the servicer's consent.

An independent accounting firm is also engaged to produce a verification report. This report certifies that the cash flows from the new securities portfolio are sufficient to meet all remaining loan payment obligations.

The transaction culminates in a formal closing, where several actions occur simultaneously:

- The original borrower is officially released from the loan.

- The successor borrower formally assumes the loan.

- The lien is removed from the real estate property.

- The new securities portfolio is pledged as the loan's sole collateral.

The borrower is then free to sell or refinance the property. The defeasance process is complete, and the CMBS trust's payments are now secured by U.S. government obligations.

Calculating the Full Cost of Defeasance

The total cost of defeasance is a complex calculation influenced by prevailing market conditions. Before initiating the process, a borrower must understand the full cost structure.

The cost is comprised of two primary components: the acquisition cost of a government securities portfolio and various third-party transaction costs.

The largest single expense is the cost of the securities portfolio. This cost is determined by the relationship between the loan's interest rate and the current yields on U.S. government securities. The objective is to purchase a portfolio of bonds sufficient to generate cash flows that exactly match the remaining payments on the loan.

The key relationship is as follows: if current market interest rates are lower than the loan's interest rate, the borrower will pay a premium to acquire the necessary securities. The new, lower-yielding bonds do not generate sufficient income on their own, so a greater face value of bonds must be purchased to meet the target cash flow requirements.

Conversely, if market rates are higher than the loan rate—a less common scenario—the portfolio cost could be less than the outstanding loan balance, potentially resulting in a net gain for the borrower.

Understanding the Securities Portfolio Calculation

Consider a loan with a $10 million balance and a fixed rate of 5.5%. If the current yield on the government securities required for the defeasance is 4.0%:

- The loan was structured to produce a cash flow stream based on a 5.5% return.

- The available market securities can provide only a 4.0% return.

To cover this 1.5% yield gap, the borrower must purchase more than $10 million in face value of securities. The total cost will be the $10 million loan balance plus a defeasance premium to compensate for the lower yield. This premium ensures the CMBS trust receives the same payment stream it would have under the original loan.

Analysis of historical deals, such as the COMM 2012-CCRE1 transaction, illustrates how these collateral substitutions are structured to ensure bondholders are made whole.

The core principle is that the defeasance must be "yield neutral" for the bondholders. The premium paid by the borrower is the cost of ensuring investors are economically indifferent to the collateral substitution.

A Breakdown of Associated Transaction Costs

In addition to the securities portfolio, borrowers must budget for professional and administrative fees. These "soft costs" are necessary for navigating the transaction's legal and financial complexities.

The typical transaction costs in a defeasance in real estate include:

- Defeasance Consultant Fee: For the firm managing the transaction from analysis to closing.

- Servicer Processing Fee: The loan servicer, representing the CMBS trust, charges a fee for reviewing and approving the transaction.

- Accountant Verification Fee: An independent CPA firm is hired to produce a report verifying that the securities portfolio's cash flow is sufficient to cover the loan's payment schedule.

- Lender's and Servicer's Counsel Fees: The borrower is responsible for the legal fees of the lender's and servicer's attorneys, who review all legal documents to protect the trust's interests.

- Borrower's Counsel Fee: The borrower will retain their own attorney to provide representation and ensure a clean release of the property lien.

- Rating Agency Confirmation Fee: In some cases, rating agencies like Moody's or S&P must confirm that the defeasance will not negatively impact the credit rating of the CMBS bonds.

The sum of the portfolio premium and these transaction costs constitutes the total financial outlay for the borrower. Obtaining a comprehensive estimate for all components is a critical first step for any borrower considering defeasance.

Evaluating Defeasance Against Prepayment Alternatives

When a commercial real estate owner seeks to exit a loan early, defeasance is not always the only method. However, within the highly structured domain of CMBS financing, it is often the sole viable option. To understand why, one must compare it to other common prepayment mechanisms, primarily yield maintenance and flat-rate penalties.

Each method aims to solve the same problem: compensating the lender for lost future interest payments. The primary differences lie in their mechanics and applicability. When a borrower has a choice, the decision depends on the loan agreement, current interest rates, and the borrower's financial objectives.

Defeasance vs. Yield Maintenance

Yield maintenance is the most common alternative to defeasance. It is a penalty calculated to ensure the lender achieves the same total yield as if the loan had been held to maturity. The borrower pays a lump sum representing the net present value of the lost future interest, calculated based on the difference between the loan's interest rate and prevailing market rates.

While both mechanisms are intended to make the lender whole, their operational differences are significant:

- Mechanism: Defeasance is a collateral swap that keeps the loan active. Yield maintenance is a prepayment penalty that terminates the loan.

- Cost: Defeasance cost is based on acquiring a specific portfolio of government securities. Yield maintenance cost is derived from a present value formula.

- Application: Defeasance is the standard for CMBS conduit loans. Yield maintenance is common for loans held by life insurance companies, banks, and other portfolio lenders.

The critical distinction is that defeasance preserves the loan for bondholders, making it structurally essential for CMBS trusts. Yield maintenance terminates the loan, which disrupts the cash flow assumptions upon which the securitization is built.

The operational complexity also differs dramatically. Yield maintenance is a relatively straightforward transaction between the borrower and lender. In contrast, defeasance in real estate is a complex process involving consultants, servicers, trustees, and specialized attorneys, typically taking 30 to 90 days to complete.

When Defeasance Is the Only Option

For most CMBS loans, the loan documents explicitly prohibit traditional prepayment, leaving defeasance as the only method for an early exit. This is not an incidental feature; it is a structural requirement designed to protect the integrity of the CMBS trust and its bondholders.

This mechanism is most prevalent in the United States but is gaining adoption in other developed markets. While less common globally, defeasance is used in mature commercial real estate finance sectors like the United Kingdom, Canada, and Australia. In Canada, defeasance is permitted in certain CMBS structures, with volume increasing from $500 million in 2020 to over $1.2 billion in 2024. The total global defeasance market is estimated at approximately $50 billion annually, with the U.S. accounting for over 80%. More detail can be found in this global real estate trends report.

The Strategic Trade-Offs

The decision to proceed with defeasance requires a careful analysis of its advantages and disadvantages.

Primary Advantages:

- Unlocks Asset Liquidity: It provides the only means to release a property from a fixed-rate CMBS loan, enabling a sale or refinancing.

- Preserves Trust Integrity: It is the only method that satisfies the structural requirements of CMBS by ensuring bondholders receive their expected cash flows without interruption.

Significant Disadvantages:

- High Potential Cost: If interest rates have declined since loan origination, the premium required to purchase the securities portfolio can be substantial.

- Operational Complexity: The process is lengthy and requires the coordination of multiple specialized parties, where any delay can be costly.

- Significant Transaction Costs: Fees for legal counsel, servicers, and consultants can add a considerable amount to the total expense.

Ultimately, the decision to defease is often one of necessity rather than preference, driven by the rigid requirements of CMBS financing. While alternatives like yield maintenance offer a simpler path for other loan types, defeasance is the purpose-built solution for extracting value from assets financed in the securitized debt market.

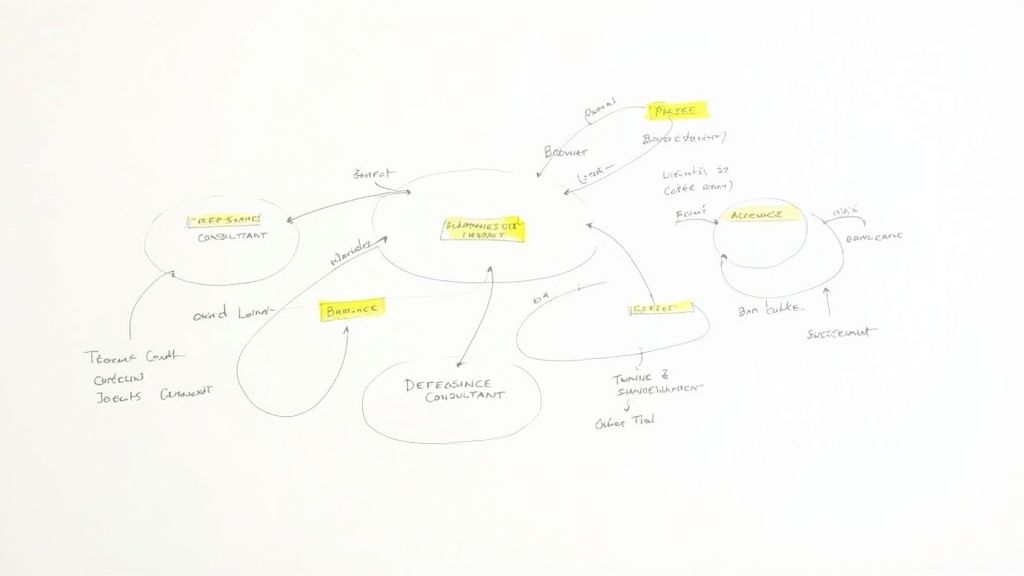

The Key Parties in a Defeasance Transaction

A defeasance is a complex transaction involving a specific cast of specialized participants. Each party has a distinct role, and successful execution requires precise coordination. Understanding this organizational structure is fundamental to understanding how defeasance in real estate functions.

The process is initiated by the Borrower—the property owner seeking to release their property from the loan's lien, typically to facilitate a sale or refinancing. The borrower is responsible for all costs associated with the transaction, from the acquisition of the securities portfolio to all professional fees.

Coordinators and Gatekeepers

Once the borrower decides to proceed, they typically engage a Defeasance Consultant. This firm acts as the project manager for the entire transaction. They provide initial cost analysis, structure the optimal securities portfolio, and coordinate communication and execution among all other parties.

Working in parallel is the Loan Servicer. The servicer represents the interests of the CMBS trust and its bondholders, functioning as the primary gatekeeper. The servicer must review and approve all aspects of the transaction, including legal documents, the securities portfolio, and the final closing structure. The transaction cannot move forward without their approval.

A successful defeasance depends on the flawless execution of each party's role. The Defeasance Consultant directs the process, but the Loan Servicer holds ultimate approval authority.

Legal and Financial Specialists

The execution of a defeasance requires specialized legal and financial expertise, bringing several other key participants into the process. A unique component is the formation of a Successor Borrower. This is a new, single-purpose entity—typically a Limited Liability Company (LLC)—created for the sole purpose of assuming the loan and holding the new securities portfolio. This legal structure formally severs the original borrower's connection to the loan.

To ensure the financial integrity of the transaction, an independent Accountant is engaged. This firm's role is to produce a verification report certifying that the cash flow from the new government securities will exactly match all remaining loan payments. This report provides the necessary assurance for the loan servicer and rating agencies. The web of counterparties in these deals can get complicated; one can get a better sense of the major institutions involved by reviewing CMBS shelf registrations.

Finally, the Trustee, acting as the fiduciary for the CMBS trust, plays a custodial role. Upon closing, the trustee takes possession of the new securities portfolio and holds it for the benefit of the bondholders until the loan's original maturity date. In addition, specialized Legal Counsel represents each of the primary parties—the borrower, the servicer, and the successor borrower—to draft, review, and execute the extensive documentation required to complete the transaction.

Roles and Responsibilities in a Defeasance Transaction

This table summarizes the primary roles of each participant in a typical defeasance transaction. Each has a defined function to ensure the process moves efficiently from initiation to closing.

| Participant | Primary Role |

|---|---|

| Borrower | Initiates the process and pays for all transaction costs. |

| Defeasance Consultant | Acts as the project manager, structuring the deal and coordinating all parties. |

| Loan Servicer | Represents the CMBS trust, reviewing and approving all aspects of the deal. |

| Successor Borrower | A new legal entity created to assume the loan and hold the securities. |

| Accountant | Provides an independent report verifying the sufficiency of the securities' cash flows. |

| Trustee | Acts as the custodian, holding the new collateral on behalf of bondholders. |

| Legal Counsel | Drafts, reviews, and executes all legal documentation for their respective clients. |

Understanding these roles is the first step in demystifying what can be a complex and intimidating process.

How Market Conditions Shape Defeasance Strategy

The decision to defease a loan is rarely made in isolation from broader economic trends. Interest rate movements and the overall health of the commercial real estate market directly influence both the cost of defeasance and the strategic rationale for undertaking it.

Defeasance volume can serve as an indicator of activity and sentiment in commercial real estate finance.

When interest rates decline, property owners with fixed-rate CMBS loans are often motivated to sell or refinance. Lower rates present an opportunity to secure more favorable financing terms or attract buyers who can. Consequently, defeasance activity typically increases as it provides the mechanism to unlock an otherwise restricted asset.

Conversely, in a rising rate environment, the economics of defeasance change. The cost to acquire the necessary portfolio of government securities can become prohibitively high, and the incentive to refinance into a more expensive loan diminishes. As a result, defeasance activity tends to slow, mirroring a general slowdown in real estate transaction volume.

The Impact of Interest Rate Volatility

Interest rate volatility introduces significant risk into the defeasance process. The cost of the required securities portfolio is calculated at a specific point in time. Minor fluctuations in Treasury yields can alter the total cost by a substantial amount.

Timing is critical.

A borrower may receive a defeasance quote, but if Treasury yields decline before the transaction closes, the cost of the securities portfolio will increase. This risk requires careful management. An experienced defeasance consultant monitors market movements closely to help the borrower execute the securities purchase at an opportune moment.

The core of a defeasance in real estate is a calculation that is highly sensitive to market movements. A small decrease in Treasury yields can lead to a significant increase in cost for the borrower, while an increase in yields could make the transaction less expensive.

Defeasance as a CMBS Market Stabilizer

From a broader market perspective, defeasance plays an important role in maintaining the stability and liquidity of the CMBS market. It provides a structured mechanism for borrowers to exit their loans, allowing loans to be removed from a pool without triggering a default or disrupting the expected cash flows to bondholders.

This mechanism is critical for the liquidity and risk management of the commercial real estate debt market. In the U.S., these transactions have contributed to the overall health of the CMBS market. In 2024, defeasance accounted for 12% of all CMBS loan prepayments, an increase from 8% in 2020. This growth highlights its importance, particularly in volatile rate environments.

The strategy is most common for office, retail, and multifamily properties, which collectively account for over 70% of all defeasance transactions. Further analysis on how market conditions are shaping the real estate outlook can be found in this report from Columbia Threadneedle.

A Look at Different Property Types

Defeasance activity also varies across different commercial real estate sectors, each driven by its unique market dynamics.

- Multifamily: This sector typically sees a consistent volume of defeasance activity, driven by strong fundamentals and frequent opportunities for owners to realize appreciated value through a sale or refinancing.

- Retail: In the retail sector, defeasance is often utilized as part of a strategy to reposition an asset, such as selling an underperforming property or refinancing a stabilized one.

- Office: The office sector has faced significant structural changes in recent years. This has led to more strategic defeasance as owners adjust their portfolios in response to evolving work patterns.

In summary, market conditions dictate the pace and economic viability of defeasance. An understanding of how interest rates, market liquidity, and sector-specific trends interact is essential for determining the right time—or whether—to use this strategy to unlock a property's value.

Common Questions About Defeasance

The complexities of defeasance often lead to recurring questions from property owners and investors. Addressing these key points is essential for anyone considering this type of transaction.

A clear understanding of these details is necessary before proceeding with the defeasance process.

Where is Defeasance Most Common?

Defeasance is almost exclusively associated with fixed-rate Commercial Mortgage-Backed Securities (CMBS) conduit loans. The mechanism is an integral part of their structure.

CMBS loans are pooled and sold to bondholders who expect a predictable stream of payments over a specified term. A conventional prepayment would disrupt this cash flow. To ensure stability, CMBS loan agreements typically prohibit prepayment, making defeasance the primary—and often the only—method for a borrower to exit the loan early and release the property from the lien.

Can a Borrower Profit from a Defeasance?

Yes, although it is an infrequent occurrence. A gain is possible if the yields on government securities have risen to a level significantly higher than the interest rate on the borrower's loan.

In such a scenario, the cost to acquire the securities portfolio needed to cover the remaining loan payments would be less than the outstanding loan balance. The borrower could potentially realize a net gain after accounting for all transaction costs.

This situation is rare and would require a sharp increase in interest rates shortly after the loan was originated. Most defeasance transactions occur when prevailing rates are lower than the loan's rate, resulting in a premium cost for the borrower.

What Happens to the Loan After Defeasance?

After a defeasance closes, the loan is not paid off or extinguished. It undergoes a substitution of collateral and obligor.

- The original property is released from the mortgage lien. This allows the borrower to sell or refinance the asset unencumbered by the original loan.

- The loan itself is assumed by a new entity, the "successor borrower."

- The loan's collateral is officially swapped from the real estate to the new portfolio of government securities.

The portfolio of bonds is then held in trust, generating payments to the CMBS trust until the loan reaches its original maturity date. The loan continues to exist, but its connection to the real estate is completely severed. This is the central function of defeasance in real estate.

Article created using Outrank